Loading video...

Emergency Funds Fail: Why Your Safety Net Might Be a Lie and What Actually Protects You

You've likely been told that emergency funds are your financial safety net. Saving three to six months of expenses feels responsible and secure. But what if this common advice is misleading? In this article, inspired by insights from Start With Cents, we'll uncover why emergency funds fail most people and how to build a true financial fortress that protects you far better than just cash savings.

Table of Contents

💸 The Hidden Truth Behind Emergency Funds

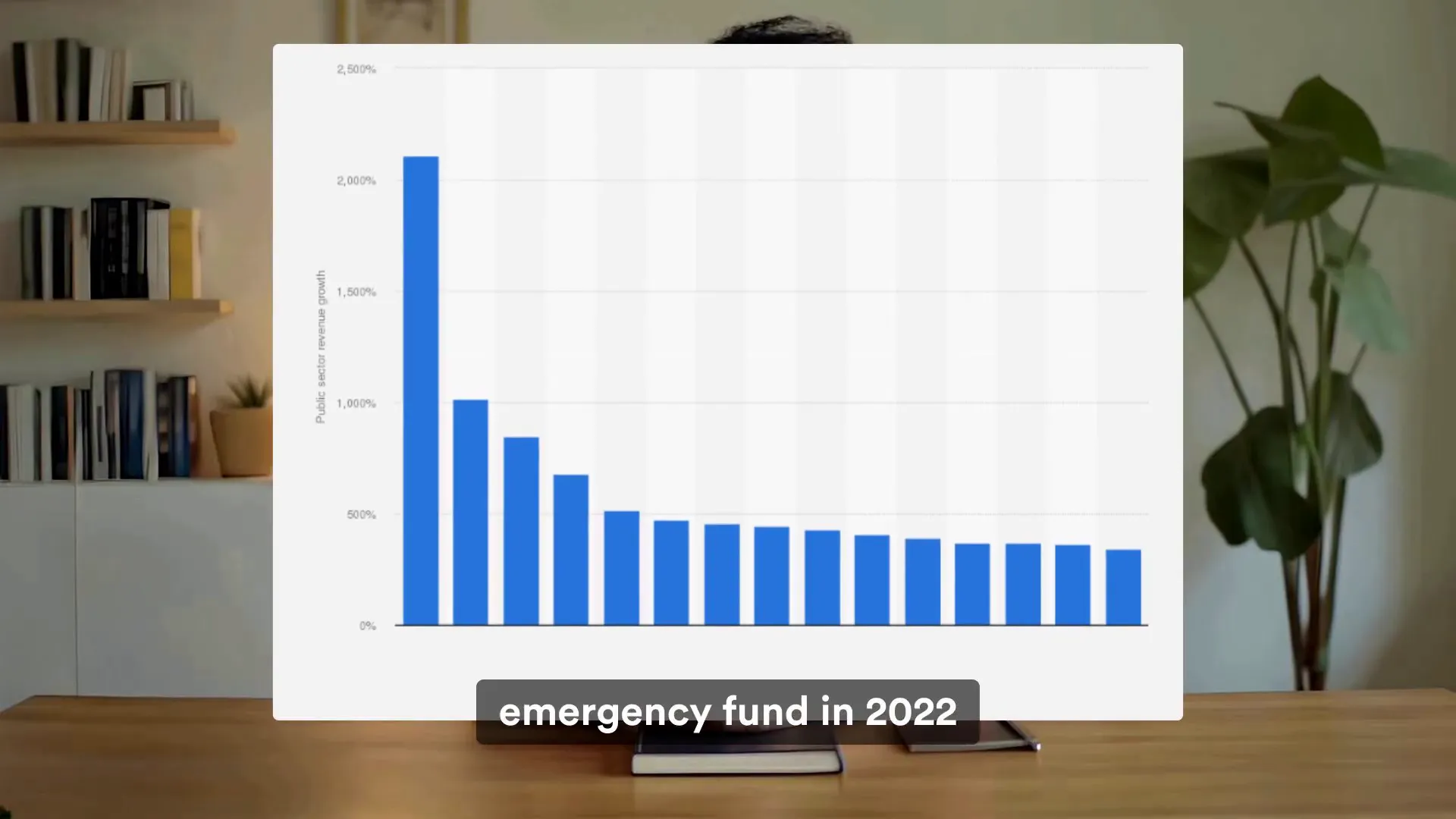

Nearly 44% of people who had a three-month emergency fund in 2022 no longer had it by 2023. Even worse, many skipped medical care and couldn’t pay their bills. Why does this happen?

At face value, saving money seems like the right move. But the harsh reality is that an emergency fund sitting in a low-interest savings account often loses value when compared to the high-interest debt many people carry. For example, if you have $5,000 saved earning about 1% interest (roughly $50/year), but owe $5,000 on a credit card charging 21% interest, that debt costs you $1,050 per year. This means you’re effectively losing $1,000 annually by choosing to save rather than pay off debt.

Think of it like filling a bucket with a tiny cup while someone else drains it with a fire hose. The bank pays you pennies, but you pay them dollars. Most financial advice says "save first, pay debt later," but the math shows every dollar in your emergency fund while carrying high-interest debt is a dollar working against you.

📈 The Lifestyle Inflation Trap

Another subtle danger is lifestyle inflation. You might save enough to cover three months of expenses, but over time, your expenses quietly grow—sometimes by 20% or more. That three-month cushion can shrink to two and a half months or less without you realizing it.

Emergency funds treat the symptom (not having money during emergencies), but they don’t fix the disease: spending more than you earn. Saving money feels good, but without addressing spending habits, it’s often a temporary bandage.

This is why 44% of people lost their emergency funds within a year—not due to bad luck, but bad strategy. Their funds sat passively while debt grew, spending habits remained unchecked, and incomes stagnated or declined.

💳 Real-Life Example: Sarah's Financial Struggle

Consider Sarah, who has $8,000 in emergency savings earning 1% interest, but also carries $12,000 in credit card debt at 22% interest. She feels secure with her savings but is losing over $2,500 yearly in interest payments while earning only $80 on her savings.

If Sarah used her emergency fund to pay down debt, she’d save $1,760 in interest payments in the first year alone. That’s more protection than her emergency fund ever provided. Yet, she was taught to save first, so she keeps losing money every day. When an emergency hits, she’ll likely use her credit card anyway to avoid touching her savings, adding more debt while keeping money that could have prevented the problem.

🏰 Building a Fortress: The Four Layers of Real Financial Protection

True financial security isn’t about hoarding cash. It’s about building multiple layers that work together to protect you. What if eliminating just $5,000 in credit card debt protects you more than saving $15,000 in an emergency fund?

Paying off debt gives you a guaranteed return equal to the interest rate on that debt—often 18% to 24%. No investment can promise that kind of profit.

Think of protecting your money like securing your home. You wouldn’t rely on just a front door lock—you’d add window locks, an alarm system, and good lighting outside. The same principle applies to your finances.

1. Eliminate Debt

Every dollar used to pay off high-interest debt instantly saves you 18-24% in interest payments. For example, paying off $3,000 in credit card debt at 22% saves you $660 annually. This is a guaranteed return that no stock market investment can match.

2. Proper Budgeting

Budgeting isn’t about restriction; it’s about clarity. Knowing exactly where every dollar goes helps you redirect funds toward financial protection. Many people unknowingly spend $200 or more monthly on unnecessary expenses.

3. Multiple Income Streams

Relying on one income source is risky. Side hustles—like freelancing, selling items online, or gig work—can replace your emergency fund’s purpose. Even an extra $500 a month adds up to $6,000 a year and can cover essential expenses during income disruptions.

4. Smart Investing for Long-Term Growth

Once debt is eliminated and budgeting is under control, start investing—even small amounts like $50 a month can grow significantly over time thanks to compound growth. This ensures your money works for you rather than sitting idle and losing value to inflation.

🛡️ How These Layers Work Together

Imagine two people:

-

Person A has $10,000 in emergency savings but $8,000 in credit card debt.

-

Person B has no debt, budgets carefully, earns an extra $400 a month from side work, and invests $300 monthly.

Who do you think sleeps better at night? Person B. They have no debt draining their wealth, clear control over their finances, diversified income, and growing investments. This multi-layered approach builds real strength and long-term security.

🔥 Why Emergency Funds Alone Are Designed to Fail

Emergency funds are not evil; they’re simply incomplete. They’re like having a smoke detector but no fire extinguisher—you get the warning but can’t stop the fire. Many people miss this fundamental point.

Start by listing all your debts and their interest rates. Create a simple worksheet to compare what you pay versus what you earn. Then ask yourself: would paying off debt protect me more than keeping cash earning 1%?

The math will likely surprise you.

❓ FAQ: Emergency Funds Fail

Q: Should I completely avoid building an emergency fund?

A: No. Emergency funds have their place, but they shouldn’t be your only financial defense. Prioritize paying off high-interest debt first, then build a small emergency fund as part of a layered strategy.

Q: How much debt should I pay off before saving?

A: Focus on eliminating high-interest debt (typically credit cards) first. Even paying off $1,000 of 20%+ interest debt can save more money than having several thousand in a low-interest savings account.

Q: Can multiple income streams really replace an emergency fund?

A: Multiple income streams provide flexibility and reduce reliance on one paycheck. While they don’t replace all emergency savings, they add a powerful layer of protection and can reduce the amount you need to save.

Q: How do I start investing if I have debt?

A: Prioritize paying off high-interest debt first because of the guaranteed return. Once debt is manageable, start investing small amounts regularly to benefit from compound growth over time.

🔑 Final Thoughts

The people who weather financial storms aren’t the ones with the biggest emergency funds. They’re the ones who eliminated the storms before they formed. Real peace of mind comes from eliminating threats, not just stockpiling cash.

Your safety net is just a lie if you don’t plug the holes. Take control by paying off debt, budgeting smartly, diversifying your income, and investing wisely. This multi-layered approach builds genuine financial security that grows stronger every day.

If this perspective opened your eyes, consider exploring more real-world finance strategies and take your next step toward financial freedom.

Subscribing really helps.

Subscribe to help me create more helpful videos for everyone's benefit.

** Subscribe to @StartWithCents **

🚀 Ready to Build Real Wealth?

You've learned the strategy – now it's time for action!

🎬 Get Weekly Financial Education

Join thousands learning smart money strategies that actually work.

📺 Subscribe to @StartWithCents

💎 Download Your Free Wealth-Building Tools

Get the exclusive "First Dollar Game Plan" – your step-by-step guide to financial freedom.

📚 Continue Your Financial Journey

Explore more money-smart articles and strategies.

📖 Read More Posts • 🏠 Homepage

💡 Remember: Knowledge without action is just entertainment. Take one step today!